7# The Tiny Shopify Remora

A closer look at WeCommerce Holdings (WE.V)

Please note that I hold shares of this company at the time of writing and none of this is a recommendation of any kind. WeCommerce Holdings is a microcap company that is illiquid (thinly traded). Please keep that in mind if you do consider investing.

This content was a collaborative effort between @MoS_Investing and I. Please check out his substack,Margin of Safety Investing, and follow him on Twitter for great content! He also holds shares of this company at the time of writing and none of this is a recommendation of any kind.

The Pitch

It trades on the TSX Venture exchange under the ticker symbol WE and on the OTC under the symbol WECMF. The company has around a 500 million dollar market cap. It has high insider ownership and grows organically and via acquisitions. It is focused on servicing the needs of Shopify merchants with software. It appears reasonably priced at the moment, especially if growth rates continue and margins continue to improve, but is not without risks; both operationally, and financially.

What is WeCommerce Holdings?

Imagine an organism that can attach itself to a host in order to coast and thrive off of the efforts of the larger, more powerful host. That’s what a Remora is.

That’s the metaphor for WeCommerce Holdings. Actually, it’s better. They are a collection of remoras. All living in the Shopify ecosystem. I don’t think I need to explain to you how wonderful and powerful Shopify has been over the past decade. It likely has tremendous growth prospects for some time to come.

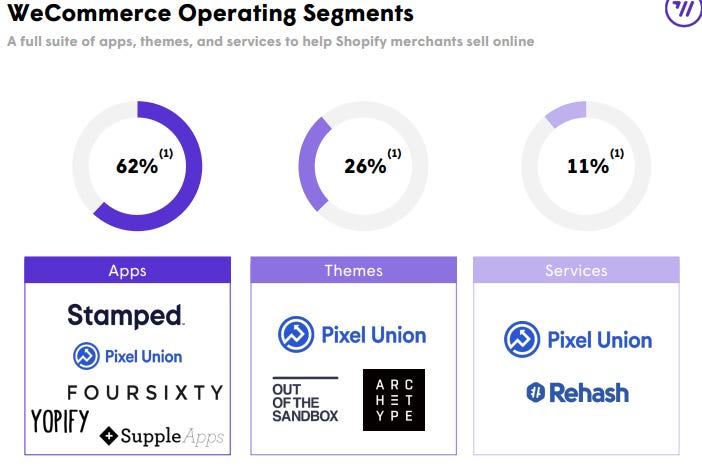

WeCommerce is a holding company of small software businesses that service Shopify merchants’ software needs. They operate in three main segments:

Themes

Apps

Services

Apps and Themes are the biggest and frankly, better businesses compared to services. This is where the focus of the business will be as the growth has been geared towards ramping up this revenue stream.

Recent data suggests about 1.75 million merchants worldwide and this number is growing at a rapid clip as of late. Shopify touts 12 Billion dollars in partner revenues. The overarching global tailwind is the 25% e-commerce growth, of which Shopify makes up a fast growing and significant market share. The penetration rate is around 5% of the whole e-commerce sector and one would assume they still have a nice runaway for growth.

Obviously, you are familiar with Constellation Software which buys at low multiples 1 to 2x revenue while WeCommerce is acquiring at higher multiples. More on acquisition later. Management has guided for 25% consolidated organic growth during their roadshow.

Management

Founder, Andrew Wilkinson is a director and owns a significant stake at 29% of outstanding shares. In all, He and founder and chairman, Chris Sparling, have years of experience with buying up small internet and software related businesses in his private holding company, Tiny. He has done well with this model and has the reps in to know how to do it well. Tiny, their digital marketing agency, acquired 30 businesses and created around $1B of value with very little outside capital or debt during the last 15 years. WeCommerce says on their website that Tiny was an “An overnight success, 15-years in the making.” which shows management focus on patience and long term-thinking.

Recently, Andrew has moved aside as chairman and stays on as a director while they have hired an outsider in Alex Persson, former co-founder of a tech investment group within Jefferies. Chris has moved from CEO to the Chairman seat.

They promote themselves as a decentralized organization which is perfect for this type of business model as can be demonstrated by the success of businesses like Constellation Software who are the poster child for the serial acquirers model.

They hired an employee of Constellation Software, Jordan Taub, Director M&A who started on November 1st 2021.

The management team also claims to have advantages for making acquisitions as they keep things simple compared to some of the competitors such as private equity. They claim to make offers to eligible sellers that fit the criteria within 7 days and close by 30 days after some due diligence. The criteria they look for is profitability, organic growth, and sticky customers.

Most recently they mentioned having 100 million dollars in annual revenue in the acquisition pipeline which, if true, is very significant compared to their current size. They look at between 750 and 1,000 companies each year and buy between three to six. The team seems to make sure to keep the culture of the businesses they are looking to acquire:

"It's really meant that we just wait for the right opportunity where there's a great founder who wants to sell their business to somebody who will understand it. And people sell to us for the same reason they sell to Buffett — because we have a great reputation. We've been doing this for 15 years, and we're founders as well. We found that a lot of private equity firms that approached us over the years kind of looked at our business like a spreadsheet, as something to flip in a few years, lock in some gains. That's not how we look at these businesses, we want to own businesses for ten, twenty, thirty years, and we want to keep the culture intact."

How a millennial's $57,700 charity lunch with Bill Ackman turned into a $46.5 million IPO

Funding Growth

Issuing stock

The company has issued stock to fund the business and will likely continue to some extent. As the business scales, they shouldn’t need to dilute common shareholders as much. Most recently, in the summer of 2021, the company raised around 33 million this way.

Balance sheet

As of the end of Q3 (October 2021) they have reported around 25 million dollars of cash and 61 million of long term debt financed at 3.625%. Liquidity stands at 48 million dollars with the unrestricted cash and leverage available with their current debt facilities. This tells you that while there is some cash available for near term acquisitions, it is not enough to fund the reported pipeline today.

Cash from operations

EBITDA can be viewed to some extent as cash that could be potentially made available to invest in the businesses for growth or for new acquisitions. As it stands today it is not a large number. The Q3 ytd stood at 8 million and even if this number grows to 10-15 million for the year, that leaves only room for a small or a few tiny add on acquisitions to move the needle over the short term. Over a five year period this could become significant in terms of being able to fund growth from cash flows from the business instead of issuing shares.

I would look for some patience and willingness to not overpay from the management team here. It will be tempting to continue the high revenue growth but the shareholders will benefit from some intelligent capital allocation for the long term value creation.

Intent to buyback shares

They announced a Normal Course Issuer Bid a few months after issuing shares. WeCommerce announced a NCIB back in September 2021 to purchase up to 1,989,000 common shares during the 12-month period ending September 21, 2022.The NCIB represents approximately 5% of the outstanding common shares.

M&A

They have done two acquisitions since becoming public which is probably not representative yet of their capital allocation but is the only indication so far:

Stamped was acquired for 10x ARR which seems a little expensive. They grow through customer addition and ARPU. There is unaudited financial statements on SEDAR from April 2021

Archetype was acquired for 5x EBITDA which seems more reasonable. WeCommerce raised prices by 70% since the acquisition so they probably paid more like 3x EBITDA. Archetype is growing through price increase.

Risks

Reliance on Shopify

This seems like the most obvious risk. While they should benefit from the continuing success and growth in the ecosystem, they also have no direct control. Basically it’s a double-edged sword. Theoretically, the ecosystem could be closed down or harmed in some ways should Shopify decide to change direction on how friendly they are to third party devs. They could also increase fees for things like the app marketplace. Although it seems unlikely, they could also do their own app and theme development, although this appears unlikely given the focus of Shopify.

Threats from competition

Competition for WeCommerce comes in two forms:

Other buyers

New developers

Other buyers could theoretically come and buy up all the acquisition targets or simply push up prices that will mean more challenges for growth via acquisitions. I think this will be a challenge with cheap money and big funds looking for a juicy slice of the attractive software businesses in the space. Theoretically, where WeCommerce can offer its targets an advantage is to be a good home for businesses that are being acquired. Autonomy and control over the operations seem to be a key to the decentralized structure that is being pitched. Couple this with the “simple and quick” pitch for selling to WeCommerce and there’s at least some chance of defending against some of the competition.

New developers starting their own businesses in the space shouldn’t be downplayed either. The barrier to entry doesn’t appear to be high. That being said, it seems likely that incumbents will have an advantage. This is because the complexity of maintaining software such as apps in a proprietary ecosystem such as that of Shopify’s that is changing (for the better normally) every 3 months.

Valuation

What are you getting for your money?

For just over 500 million dollars you are getting close to 50 million in sales with around 20%-30% EBITDA margins. With sales growth quite high (90% quoted in Q3 2021) and with little reason that slows too quickly, it would seem you are paying somewhere around 30-40x EBITDA and around 10x Revenue today.

The valuation to properly consider future growth needs to consider how the growth will be funded. Some dilution will not hamper returns too much but I would want to see the bulk of the growth going forward be purchased with cash from operations and from some reasonable debt financing instead of sales of stock.

The SaaS premium

Another way to value the business is to compare to similar businesses. If you look at what is happening to the three revenue streams, it appears that the apps recurring revenues are taking a lead and one can read between the lines that that is likely the future form of the business model. If you apply a multiple for fast growing saas of say 15-20x sales (larger fast growers are currently trading at much higher multiples but could also have stronger moats) and project out sales to double or triple in the next few years, you would then get to a market cap of 1-2 billion. It’s very likely that dilution will occur to get there, especially if done quickly. Even if you get diluted by 2x, you could still generate very good returns if the organic growth and industry tailwinds continue in the upward direction for the next 5 years.

Comparable valuation

Here is a list of public companies in the software consolidators sector which could be used to compare relative valuation. WeCommerce could show some upside on a NTM EV/EBITDA or NTM EV/Revenue.

Image courtesy of @Antoine

Analysts expectations

There are two analysts currently covering WeCommerce

TD Securities analyst as of November 23rd, 2021, is maintaining buy rating with a $22 target price. They used an EV/Revenue multiple based on revenue estimate of $64.5mm in 2022, $25mm of M&A at a 3.7x FWD Revenue and an EV/Revenue multiple of 13x on organic and acquired revenue.

Canacord analyst as of November 23rd, 2021, is also maintaining a buy rating with an $18 target price based on 13x EV/2022E Revenue multiple.

Ownership

Insiders own approximately: 61%

Institutional and Mutual Funds own approximately: 10%

Recent insider transactions:

During December 2021, the former Chairman, Andrew Wilkinson, and the new CEO, Alex Persson, bought shares. Shane Parrish, a director on the board, sold around 25% of his holdings .

You can support my work by buying me a coffee or whatever donation you feel like:

Thank you for your support!

| A guest post by

|

It will be a bit disappointing if they do no buybacks in C2Q. That will be something to watch for in upcoming results.

Very interesting writeup. Hard to fully understand the decline YTD. General ecomm weakness, doubts about the future of the Shopify platform, general de-rating across software/internet multiples?

You would think it is very interesting here. The biz prob trades well below the value of all its M&A. It is starting to look reasonably valued on just the underlying FCF with no value attributed to future M&A (looks like mid teens runrate FCF). And valuations of potential deals are way down, improving the NPV of future deals.

Have there been any negative fundamental developments that help explain the selloff?